More than half of Americans—and in some surveys, nearly two-thirds—say their pay isn’t keeping up with prices. Despite nominal wage growth, inflation and rising living costs continue to erode purchasing power. This structural squeeze is fueling financial stress, prompting many to reevaluate their careers, negotiate for raises, or seek supplemental income.

The Hidden Crisis: Pay vs. Cost of Living

When we say “52% of Americans say their pay isn’t keeping up with prices,” we’re not exaggerating—but the reality behind that number is nuanced. Surveys from institutions like Bankrate show that a growing majority of workers feel financially squeezed, even as official statistics sometimes paint a different picture.

This disconnect between how people feel and what economic indicators say comes down to real purchasing power—what your paycheck can actually buy after factoring in inflation.

Why It Feels So Hard to Get Ahead

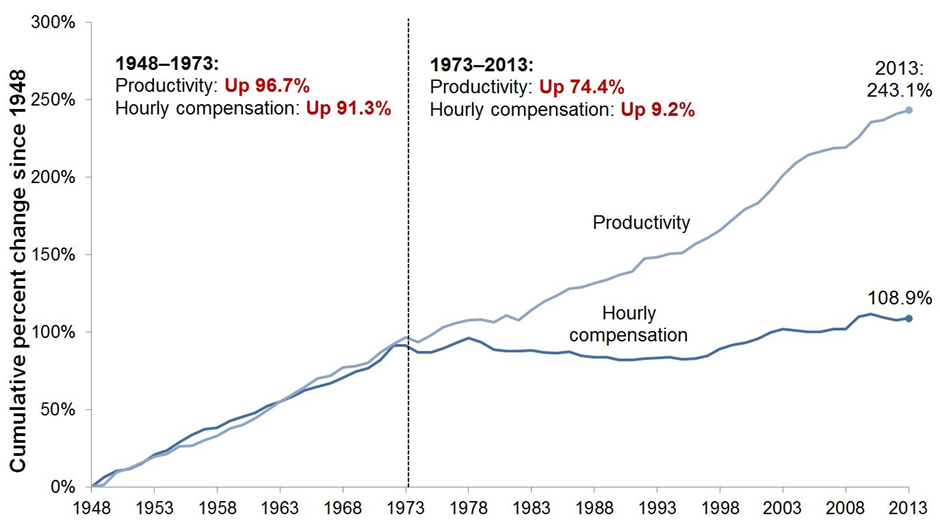

Real Wage Gains Are Smaller Than They Appear

According to Bankrate’s Wage-to-Inflation Index, wages have outpaced inflation recently, but workers are still down roughly 1.2 percentage points in total purchasing power compared to early 2021.

For example: someone making a $50,000 salary with a 4% raise may feel better on paper, but if inflation is still 3–4%, that improvement barely moves the needle when it comes to everyday costs.

Inflation Isn’t Evenly Felt

The Census Bureau uses a “chained” CPI (C‑CPI‑U) to adjust for inflation when estimating real income. In 2023, real median household income rose to $80,610, a 4% increase from 2022. But that still may not feel like enough when certain costs—like housing, healthcare, and childcare—are rising faster than average.

Raises Aren’t Always Enough

More than half of workers who did get raises still say it wasn’t enough to match inflation. According to Monster’s survey, 95% of workers say their pay hasn’t kept up with the cost of living. Cost-of-living adjustments (COLAs) remain rare — many pay raises are merit-based rather than pegged to inflation levels.

Real-Life Stories: How Americans Feel the Squeeze

● Emily, a mid-30s teacher in Ohio, received a 3% raise this year. Great, right? But her rent, utilities, and grocery bills rose more than 5%. She now finds herself dipping into savings just to make ends meet.

● Carlos, a software engineer in Texas, left his job to freelance. Even though he makes more hourly, he doesn’t get health benefits, and he worries about long-term stability—especially with inflation still a threat.

● Janet, nearing retirement in Florida, says she’s barely treading water. Her salary has ticked up, but so have property taxes, insurance, and medical costs. She wonders if she can rely on Social Security later.

Why So Many Americans Are Saying “No” to “Is My Job Enough?”

Structural & Economic Drivers

- Stagnant Pay Adjustments: Traditional pay increases don’t account for rapid cost-of-living increases.

- Unequal Inflation Impact: Prices for essentials—housing, food, medical care—are rising faster than many discretionary goods.

- Savings & Debt Trade-Offs: To cover shortfalls, people are cutting spending, delaying major life goals, or tapping savings and credit.

- Limited Mobility: Job switching has historically been a way to boost pay, but surveys indicate fewer people are doing it.

- Psychological Toll: The financial strain affects not just wallets, but wellbeing—leading to stress, burnout, and even career shifts.

What Can You Do if You Feel Underpaid? (Actionable Advice)

● Track Your True Budget: Use a detailed budgeting tool like Mint or YNAB to see exactly where your money is going. Identify recurring expenses that may be eating your purchasing power.

● Negotiate Smart: When asking for a raise, don’t just talk about performance—bring data on inflation, cost of living, and market rates.

● Explore Alternative Income: Side gigs, freelance work, or monetizing your skills can help bridge the gap—but weigh the trade-offs (e.g., benefits vs flexibility).

● Build an Emergency Cushion: If you don’t already have one, try setting aside 3–6 months of living expenses. Even in tight times, this reduces anxiety.

● Advocate Collectively: Whether through unions or employee groups, there’s power in collective bargaining for COLAs or better compensation.

● Invest Wisely: If you have spare funds, consider inflation-hedged investments (like TIPS) or high-yield savings accounts to preserve your purchasing power.

Broader Implications: Why This Trend Matters

● Talent Retention Risks: Companies that don’t adjust pay effectively risk higher turnover, especially among skilled workers.

● Economic Inequality: Those at the lower end of the pay scale are more exposed to the squeeze—widening the wealth gap.

● Policy Pressure: Persistent wage stagnation could drive public demand for minimum wage increases, better tax credits, or other reforms.

● Consumer Behavior Shifts: As workers spend less or save more, consumer demand could shift—impacting everything from retail to housing markets.

Frequently Asked Questions (FAQs)

- Why do some reports say wages are rising faster than inflation, but people still complain?

Official wage growth doesn’t always reflect real purchasing power. If inflation is high, small raises may not keep up with the actual cost of living. - Is the “52%” figure reliable?

While the exact number can vary by survey, multiple sources suggest that more than half of U.S. workers feel underpaid relative to inflation. - Are all workers feeling this, or just certain groups?

The squeeze is broad, but it’s especially acute for older workers (Baby Boomers) and middle-income earners. - Have wages ever kept up with inflation in the past?

Historically, there have been periods of stronger real wage growth—but since the early 2000s, gains have been uneven, especially for middle- and lower-income workers. - Why don’t more companies offer cost-of-living raises?

Many companies still tie raises to performance, not inflation. Granting COLAs can be expensive and complex, especially when inflation is volatile. - Can switching jobs really help?

Yes, historically, job switching has been one of the fastest ways to get a big raise — but recent data suggests that premium is narrowing. - What role does monetary policy play?

Central banks raise interest rates to curb inflation, but high rates can also tighten labor markets and slow wage growth. - Is this just an inflation problem, or something deeper?

It’s both. Inflation is a major driver, but structural factors (like wage-setting practices, economic policy, and market power) also play a big role. - How do taxes and benefits affect this picture?

High taxes, rising healthcare costs, and shrinking employer benefits can erode take-home pay even more — compounding the perceived shortfall. - What should policymakers do?

Potential solutions include: expanding earning-based tax credits, incentivizing COLAs, raising the minimum wage, and increasing support for affordable housing and healthcare.

Key Takeaways

● A significant portion of Americans feel their pay isn’t keeping up with the rising cost of living—even if nominal wages are going up.

● The gap persists because real wage growth (accounting for inflation) has lagged for many, especially at certain income levels.

● The consequences are real: increased stress, tapping savings, job shifts, and rethinking financial plans.

● But it’s not hopeless: budget better, negotiate smart, explore supplemental income, and advocate for change.

● Broader systemic reforms (pay policy, inflation adjustments, labor protections) will be critical to addressing this challenge at scale.